search the site

Thinking outside the boxThe global logistics business is going to be transformed by digitisation

Thinking outside the boxThe global logistics business is going to be transformed by digitisation

This will be bad news for some

THE Munich Maersk, which entered service in June 2017, is a testament to the technological marriage of information and transportation. Its bridge looks like a very spacious cockpit. Packed with computer screens, it is all glass, no brass—with a wheel that looks more like a pilot’s control column. Sailing her 214,000 tonnes from port to port takes a crew of just 28. Loading and unloading the 20,000 containers she carries only needs the supervision of one crew member.

The Munich Maersk, though, is a high-end exception—one of the best ships in the up-to-the-minute fleet of the biggest shipping company in the world. It shows what can be done. But at the moment the industry’s big issue is what is being left undone.

Between 1985 and 2007 trade volumes rose at around twice the rate of global GDP. In the 1990s the world’s largest container ships only had space for 5,000 or so containers; now it boasts giants like the Munich Maersk. The global logistics industry had revenues of $4.3trn (€3.3trn) in 2014, according BCG, a consultancy.

But though the flows and the pipes have got bigger, the principles of the industry’s plumbing have changed little since they took their modern form in the 1950s and 1960s. Use containers of standard sizes that can be loaded onto trains, lorries or ships as needed; use scale to cut costs; co-ordinate the whole thing with a physical paper trail. When in doubt, buy something bigger.

The economic slowdown following the global financial crisis hit this way of doing things hard. Although giants like Maersk continued to buy enormous ships, smaller lines with worse balance-sheets could not. Airbus, which had hoped to sell a freighter version of its A380 superjumbo, abandoned its plans. Freight rates plunged as demand for shipping did not keep up with supply. Between 2012 and 2016, the Shanghai Containerised Freight Index, a measure of prices, fell by 73%.

At the same time, the growth of e-commerce saw more aware, more demanding corporate customers insist on ever better handling of what is called logistics’ “last mile”—moving purchases from their distribution warehouses to the people who bought them. Though today’s talk is all of delivery drones and driverless vans, the key to this transformation has been not new equipment but new ways of handling data: knowing where hundreds of millions of things are and where they are going, and being able to act on that data as things change.

Now companies that have been crucial to these changes at one end of the distribution chain—Alibaba and JD, which are Chinese, and Amazon, which is American—are eyeing the rest of it. The business of moving goods internationally from factory to factory and warehouse to warehouse requires many more capabilities than shifting items from local warehouses to doorsteps. But it also accounts for 90% of the logistics’ industry’s global revenue. How far the intruders can displace the incumbents and what new business models come out of the struggle will help determine how much world trade can grow and who the winners and losers from that growth will be.

Adrift in a sea of paper

Firms looking to move components through their supply chain or finished goods to retailers have two main options. Express-delivery services such as DHL Express (part of Deutsche Post DHL), FedEx and UPS are fast and flexible—all the more so now they have embraced new data-management systems. But they are also expensive—especially for long-distance air freight. Shipping a 70kg parcel from Shanghai to London with DHL Express takes three times longer, and costs four times as much, as buying a human of the same weight an airline ticket. The passenger gets a baggage allowance and free drinks, too.

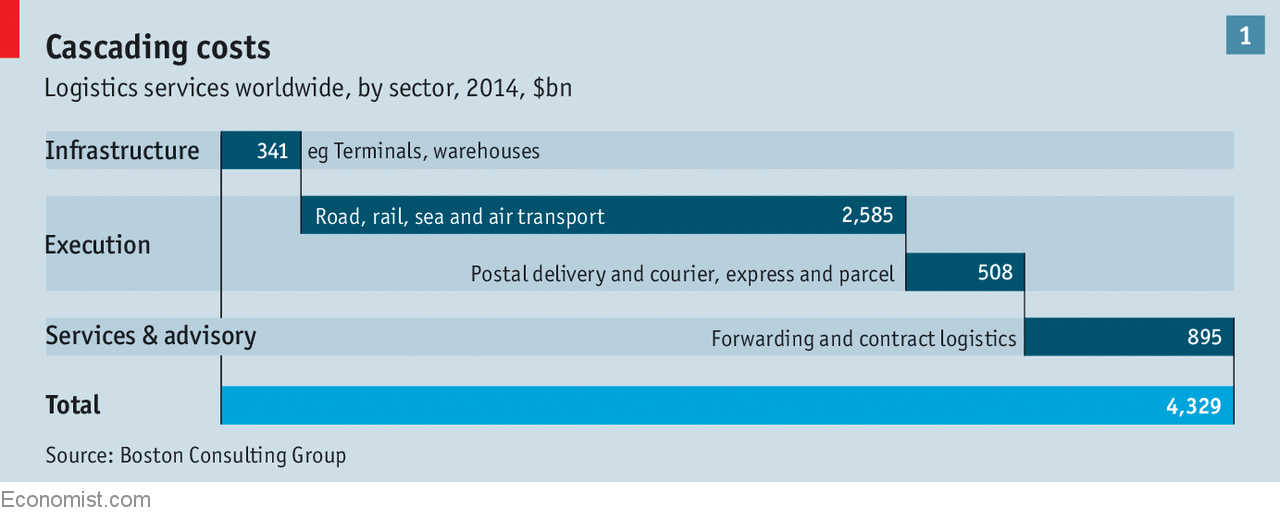

So most goods wend their way across the world using the second option—containerised freight. The non-domestic cargo business has revenues of $2.6trn a year, according to BCG. And a lot of those revenues go to middlemen. Dealing with customs clearances, insurance, transfers between sea and road and rail and all the other physical, procedural and bureaucratic hold-ups that freight is heir to requires the services of a freight forwarder. These companies account for over a fifth of the logistics industry’s revenues (see chart 1); in some cases they receive as much as 45% of the total delivery cost. In 2016 Deutsche Post DHL’s in-house freight-forwarder made over $26bn in revenues. Its smaller rivals Kuehne + Nagel, of Switzerland, and DB Schenker, of Germany, made $20bn and $17bn respectively.

For the most part, freight-forwarding companies charge a percentage of the total cost of the shipment; this gives them little incentive to drive costs down. In a free and transparent market where all the shipping options were easily discoverable, this problem would be solved through competition. But the complicated world of shipping contracts is a long way from that ideal, and the incumbents have clear reasons for keeping it so. Zvi Schreiber, founder of Freightos, a website headquartered in Hong Kong that is introducing some transparency by allowing users to compare and book different options, says many firms may take two or three days to quote a price for taking an air-freight pallet or a shipping container from A to B. And forwarders are often unable or unwilling to say whether the goods will get from China to Europe in one month or two.

The industry’s backwardness can be seen in its thrall to paperwork. Systems based on e-tickets that say who is entitled to go where, and how, have been mandatory in air-passenger transport for ten years. But half of air cargo still travels with paper “bills of lading” rather than e-tickets. In the world of containerised shipping things are even worse: freight forwarders deal with shipping firms, airlines and hauliers mainly by fax. The cargo on each voyage of the Munich Maersk generates a library of documents—many of which then need to be sent to the ship’s destination by some other means. That secondary shipping is not foolproof, either: vessels and aircraft are often delayed in port because the paperwork has not caught up with the goods that they carry.

The cost of all this is enormous. Removing administrative blockages and outdated practices would, by some accounts, do more to boost international trade than eliminating tariffs. The UN reckons that putting all the Asia-Pacific region’s trade-related paperwork online could slash the time it takes to export goods by up to 44%, cut the cost of doing so by up to 31%, and boost exports by as much as $257bn a year.

The burden is felt throughout business. Two-thirds of the American importers who responded to a recent survey undertaken by Freightos said that over a quarter of their deliveries from abroad arrive late. Some 42% said they spend more than two hours on paperwork to arrange a shipment. And 83% said they struggle to track items as they move across the world. That leaves many frustrated. “Amazon Prime can deliver to your house from its warehouse at a set time,” Mr Schreiber says. “Why can’t you do the same with air and sea freight?”

One answer is regulation; there are a lot of institutional obstacles to reform. For instance, in 2008 a UN convention put electronic documents in international shipping on a firm legal footing. But for these “Rotterdam rules” to come into force, the agreement must be ratified by 20 countries. Owing to a lack of interest in the subject among politiciansthe tally so far is just four: Cameroon, Congo-Brazzaville, Spain and Togo.

Poor communications used to be partly to blame, too, but that excuse has fallen overboard. Inmarsat, a company originally set up by the International Maritime Organisation to provide satellite services for ships at sea, today offers data rates for ships that are over 100 times faster than they were 20 years ago. Various companies rushing to provide new mobile-broadband services will improve things further. Not just ships and planes, but the individual packages and containers within them, can increasingly be tracked in real time.

The Cincinnati kids

Such data can help integrate the legs of a journey, for example by making sure that lorries do not wait for a ship that is behind schedule, or that they arrive early for one that’s ahead. They open the possibility of redirecting items along quicker or cheaper routes as they become available—if the shipper can find out about them.

The hard-to-get information which lets people find spare shipping capacity will power the real revolution, according to Martin Stopford of Clarksons, a shipbroker. Matching spare capacity to cargo in need of transport on the fly would allow the “Uberisation” of the freight business. There are already signs of this in haulage. America’s lorries travel empty more than a quarter of the time: the wasted capacity is equivalent to 200,000 lorries travelling 1,000km every day. This is because it is hard for forwarders to find return cargoes using phone or fax. Now apps have appeared to match loads with drivers, just as the Uber app pairs passengers and drivers. Indeed Uber Freight is one of the contenders. Cargomatic, a startup based in Los Angeles, and Trucker Path, a rival in Texas that was bought by a Chinese firm in December, are competing with it for the freight business, while Amazon is testing “Amazon Flex” as a way of getting gig-economy drivers to make deliveries.

The vision of many in the industry is that such services will eventually cover all sorts of different transport modalities all over the world. In the past, realising the benefits of an integrated global network of ships, planes and lorries required owning such a network, a task too big for even the largest logistics firms. Maersk, one of the world’s largest container-terminal firms as well as its largest containership operator, ran its sea- and road-logistics businesses almost entirely separately until 2016. Most companies chose to specialise and hand co-ordination over to the forwarders. Smartphones and sensors mean that, with the right platform or platforms, a freight forwarder, or a tech firm that had taken on such a role, could co-ordinate things much better than is possible today—and without any faxes.

One of those seeking such changes is Amazon. In 2017 it spent $25bn on logistics. It thinks it could get better value for money by expanding what it does itself from last-mile to all-the-miles. It has created its own logistics division and acts as its own freight forwarder. Its cargo airline, Amazon Air, is still a tiddler compared with FedEx, with just 33 jets in its fleet. But the cargo hub in Cincinnati on which the company is spending $1.5bn will have room for 100 jets. It has also been granted a licence to act as a maritime freight forwarder.

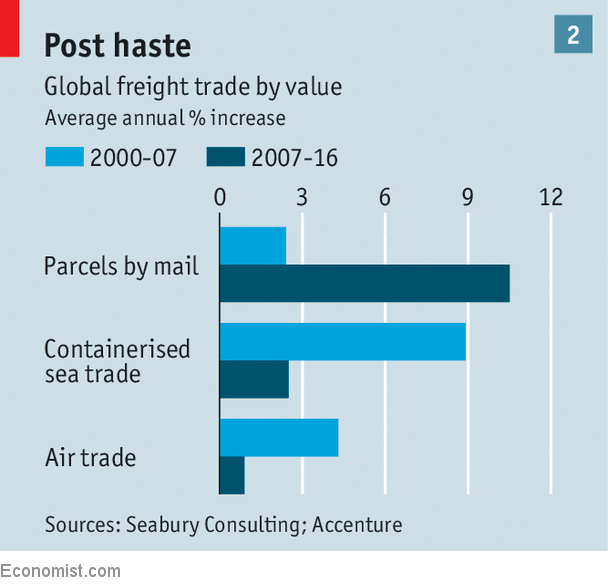

Freight forwarders and transport giants alike claim that they do not see Amazon’s move into logistics as a threat. The explosion of e-commerce (see chart 2) allows DHL, FedEx and UPS to tell shareholders happy stories about their future. The demand for parcel delivery is growing by more than 7% a year, sufficient both to maintain jobs and survive competition, according to Frank Appel, the boss of Deutsche Post DHL. Automation may mean it will soon take a third fewer people to deliver a given volume of goods, he says—but the increase in demand will still make the industry a net job creator. And it will also mean that there will be room enough for both DHL and Amazon to grow.

Another reason for such optimism is that, so far, Amazon has mainly used its network to serve its own customers. But that will change. The companies with big e-commerce networks are keen to take on other firms’ logistics, too. The idea is not to own all the ships and rolling stock—though they may own some particularly profitable bits of the system—but to control the platforms that make services available, and to bring the rest of the industry on board by simply being too big to refuse.

Perhaps the furthest down the road in this respect is Alibaba. Alibaba is a digital platform where buyers and sellers meet, rather than a retailer that holds inventory itself. It has thus always been focused on end-to-end logistics in a way that Amazon, which runs most of its business through warehouses to which goods are delivered by normal channels, is not. Alibaba says that last year it was the middleman in $550bn of transactions within China, serving over 500m customers. Through its logistics platform, Cainiao, it delivers 70% of all e-commerce parcels in China.

Now Alibaba has its eyes set on international e-commerce. A study produced by Alibaba’s research arm and Accenture, a consultancy, in 2016 predicted that cross-border e-commerce shipments worldwide could rise from $400bn in that year to nearly $1trn by 2020. Until recently, these international shipments tended to be restricted to fairly high-value goods. But Alibaba now ships cheap, bulky things like nappies and milk powder from manufacturers in America to consumers in China. Last September the company said it was going to invest $15bn in boosting Cainiao’s cross-border capabilities.

These developments should increase the total volume of goods shipped around the world yet further. But Rob Wolleswinkel of BCG counsels against seeing this as a rising tide for all boats. Amazon’s logistics division, he suspects, will seek to “cherry pick” profitable undertakings such as managing the system, leaving only low-margin activities, such as basic transport services, to the likes of Maersk and DHL. The newcomers, he notes, have two things on their side that previous would-be disrupters did not. One is that the company that owns the data owns the consumer. Amazon knows a great deal about the people who use its platform, which is a lot of people; logistics firms know next to nothing about anyone. Second is the size of the tech giants. DHL, FedEx and UPS have been big enough to bat away competition from startups. The e-commerce titans are another matter.

Some have woken up to the threat. Soren Skou, chief executive of Maersk, argues that it was a mistake for his firm to spend the past decade focusing so much on no-frills container freight between China and Europe. That allowed freight forwarders to scoop out the profit that Amazon and Alibaba now covet. Maersk must become more integrated to compete against Amazon, he says: he wants to make it “the DHL of the sea,” offering worldwide door-to-door delivery. He plans to replace paper bills of lading with digital ones secured using blockchain technology. The firm is already rolling out a digital “Maersk Line Operating System” to put shipping data into a common format. This promises to be hugely influential. As an executive at a smaller rival admits: “We just watch what Maersk does and copy it.”

Et TEU, Brute

In the past, the unreliability of container delivery has made it unsuitable for e-commerce; that has been good for other retailers, who can turn a profit importing items from China in bulk to Europe and America and selling them on. If Maersk, or anyone else, can make containerised shipping truly responsive and flexible it will have implications well beyond logistics.

It might seem fanciful to think of shipments on a behemoth like Munich Maersk being flexible in the way that vans tootling round suburbs with packages can be. But smart data management and good data analytics might get you a long way towards the goal. If you really know where all the goods are and have control over where they will go, you do not necessarily need to wait for an order before you ship something. If you know roughly how many of the items in question the market is interested in, they can be shipped ahead of time, their e-ticket-like labels left deliberately vague. When an order is actually placed, the relevant label will be updated with a precise destination in transit. The ship takes on part of the job of the warehouse. Alibaba and Amazon are already pursuing this approach.

To the extent that it can be made to work, such magic will eat into retail and wholesale margins—which for books and toys can be over 50% of the price. This is already happening to some extent. In 2012 Amazon began to allow Chinese businesses to start selling through its marketplace programme, which fulfils third-party orders; they now outnumber American firms. And Amazon has slashed the cost of delivering small items ordered from China to America. It is now lower than the cost of shipping within the United States (though delivery is slower). Other American retailers, online and off, are angry at what they see as a subsidy to their competitors.

Some estimate that as many as 7.5m retail jobs will disappear in America over the next decade, in part because of the increased possibilities for e-commerce that better logistics will bring. Others are more optimistic. Michael Mandel of the Progressive Policy Institute, a think-tank in Washington, DC, has pointed out that in America jobs in logistics are increasing faster than retail employment is falling. Those new workers, though, are unlikely to be employed by old firms. As Mr Stopford notes, incumbents did badly last time technological change swept logistics. “Who today has heard of Blue Funnel Line?” he asks of the British firm which was one of the largest cargo lines in the world—before containers and Maersk came along.

Featured Post

The hijacking of M.V. Abdullah

The hijacking of M.V. Abdullah The hijacking of M.V. Abdullah By Ghulam Suhrawardi* Since the first hijacking of Bangladeshi vessel M.V. Jahan Moni in December 2010, M.V. Abdullah was the second vessel to encounter the same fate on March 12, 2024. KSRM Group, the parent company of SR Shipping Limited, owns both vessels. Based on […]

Candidates for Secretary-General of IMO

Candidates for Secretary-General of IMO Candidates for Secretary-General of IMO in International Shipping News 04/04/2023 Seven IMO Member States have each nominated a candidate for the post of Secretary-General of the International Maritime Organization (IMO). The term of the current incumbent, Mr. Kitack Lim of the Republic of Korea, expires on 31 December 2023. The nominations received […]

RECENT JOB OPENINGS